DeepDive: The Latest from the PBoC

In our DeepDive, we analyse the PBoC’s latest macroeconomic outlook. Our text-based macro indicators continue to point to an improving outlook, reinforcing our cautiously optimistic view that we adopted in early February. Our DeepDive has the latest readings of our indicators and key messages from the PBoC’s policy communication.

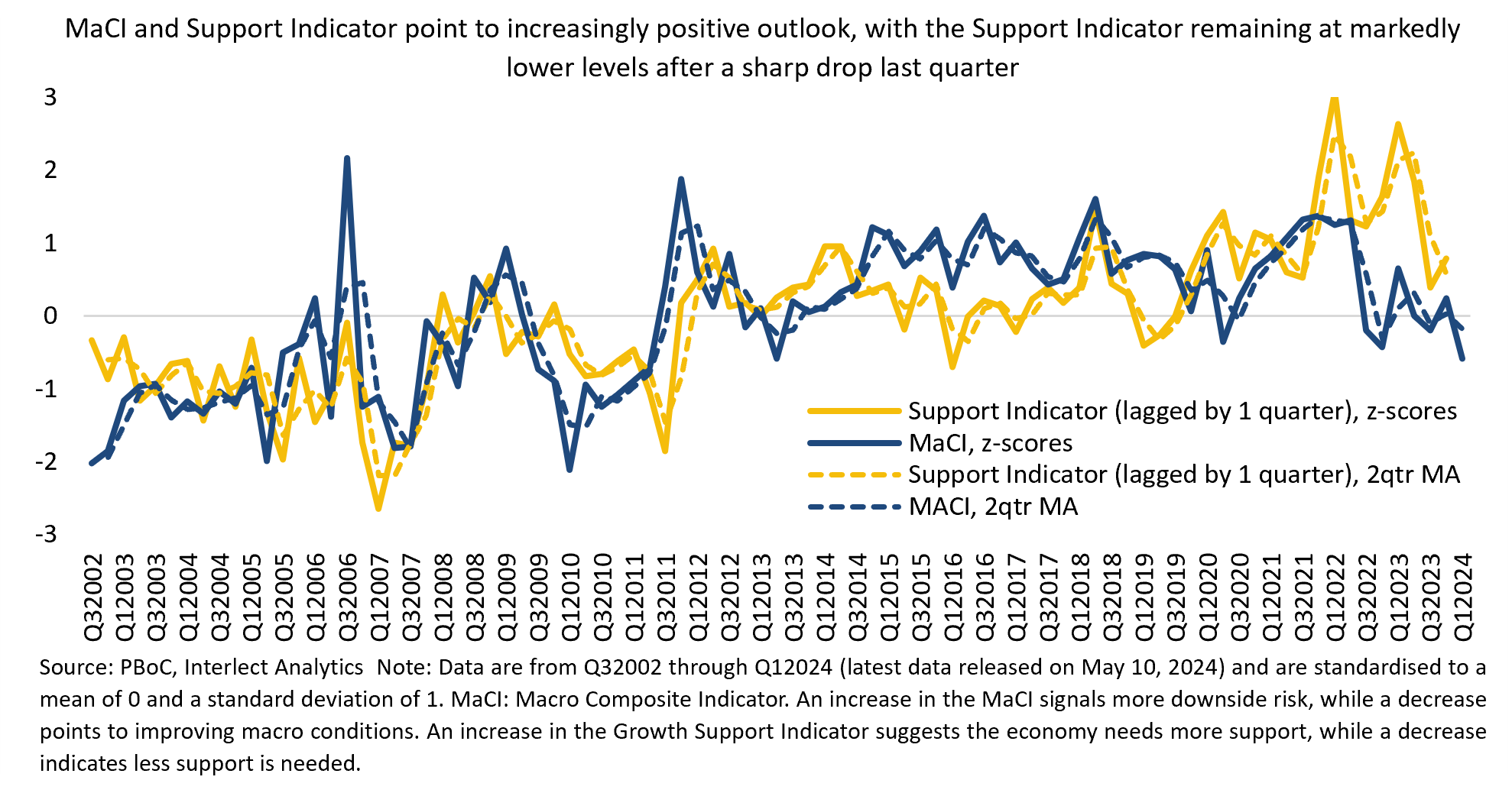

Our text-based Macro Composite Indicator (MaCI) has dipped below its long-term average when applied to the PBoC’s macroeconomic and monetary policy outlook. This trend is further supported by our growth support indicator, which remains at markedly lower levels compared to 2021-2023, following a significant decline in the last quarter (see chart). Historically, lower readings on these indicators tend to signal improving macroeconomic conditions, with implications for a range of asset classes (see below).

The MaCI, which is sensitive to textual references indicating risk and weak economic activity, and the growth support indicator, which responds to topics signalling the economy requires more support, have historically moved in lockstep, with the support indicator trailing the MaCI by about one quarter. In 2022, however, the two indexes diverged sharply, likely due to less straight forward policy communication on economic weakness, which the MaCI is more sensitive to. This divergence made us skeptical regarding the macroeconomic outlook. It also made the growth support index an important ‘countercheck indicator’ against the MaCI when communication on economic weakness gets murky.

The two indicators began to converge again earlier this year, suggesting that signals given by the MaCI on its own should carry greater significance again (also see QuickScan: The PBoC’s Optimistic Outlook for details on the relation between the MaCI and growth support indicator and New Set of Text-Based Macro Indicators for a comprehensive introduction of our suite of text-based indicators). The latest readings reinforce our cautiously optimistic outlook, which we adopted in mid-February this year, although structural issues remain.

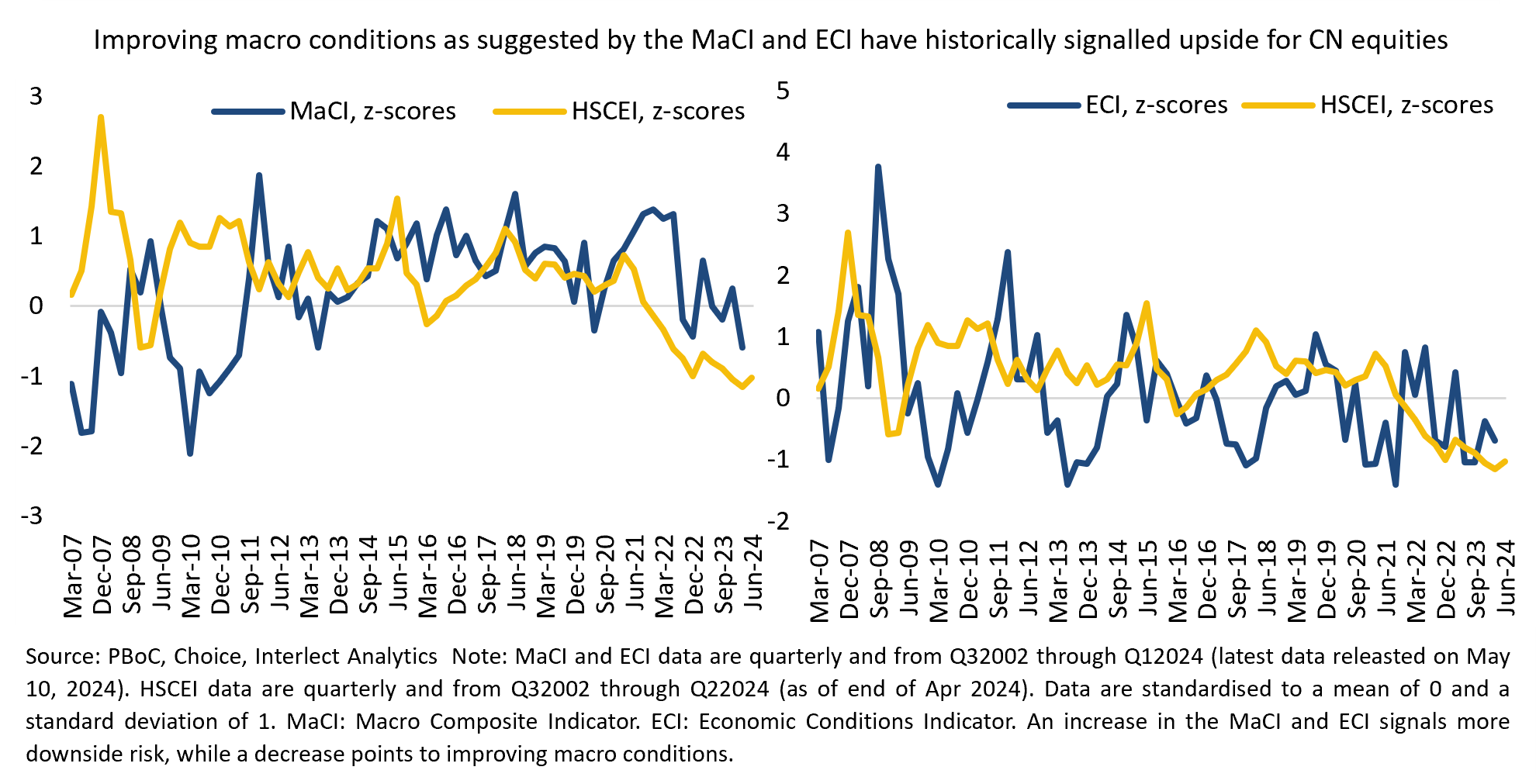

A lower MaCI and ECI, a sub-index of the MaCI, have historically tended to be good news for Chinese equities (see chart).

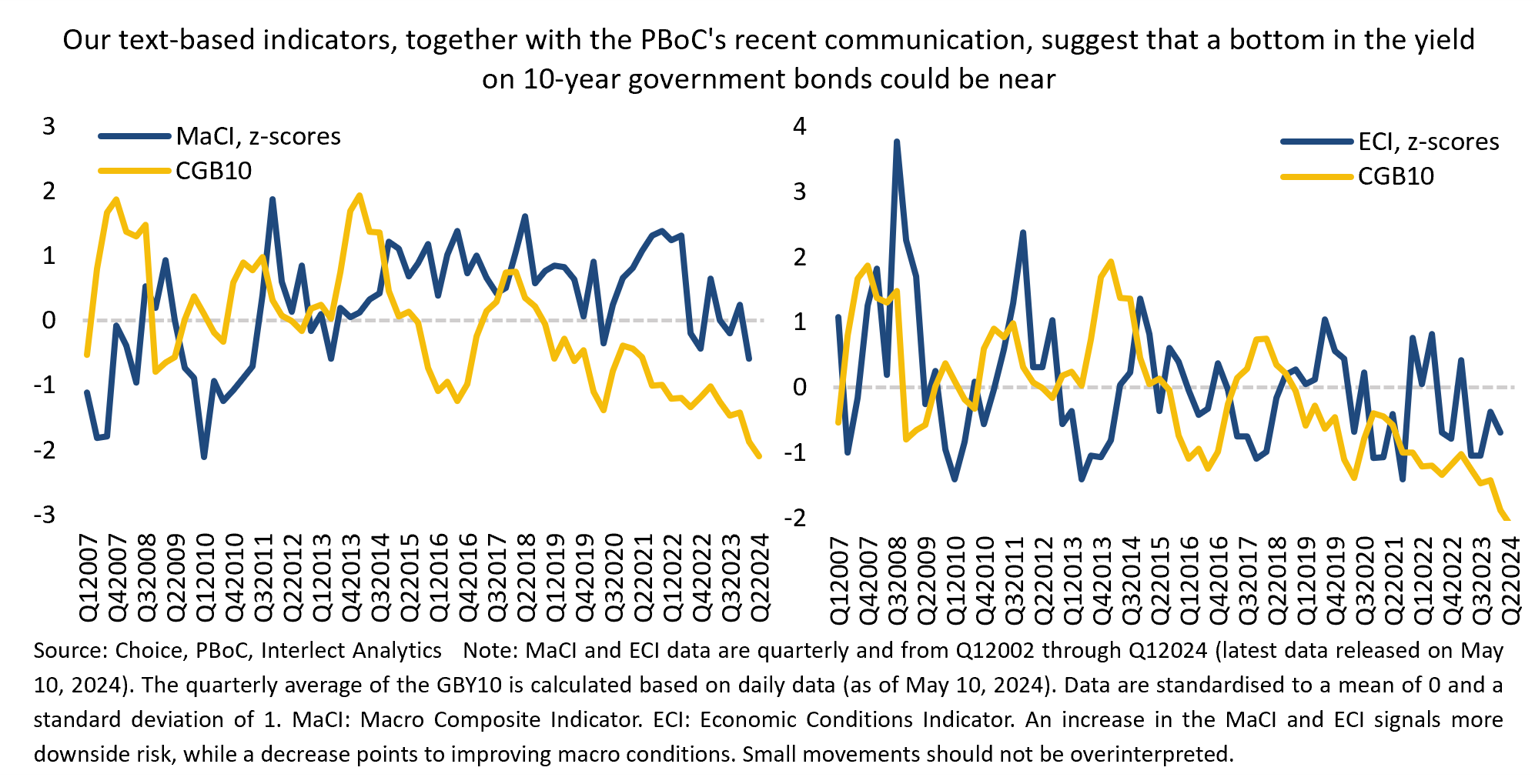

Lower readings on the MaCI and ECI have typically also had negative implications for long-term bonds (see chart). We continue to believe that the readings, coupled with the PBoC’s recent communication, suggest headwinds for the bond bull market may be ahead (see QuickScan: Watching the Long End of the Curve).

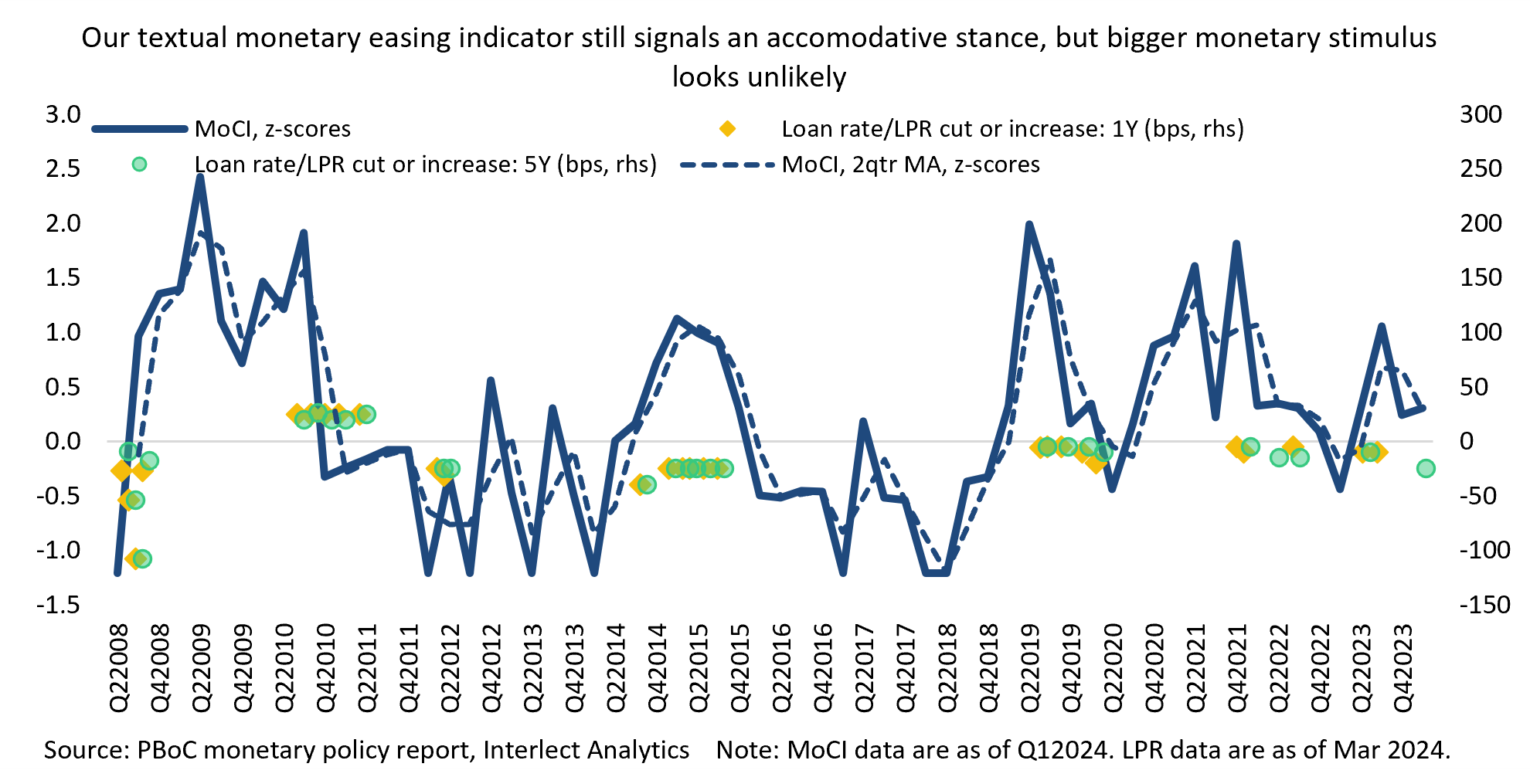

In DeepDive: Politburo Update April 2024, we noted that the recent Politburo meeting was unusually specific in singling out the flexible use of interest rate and bank reserve requirement cuts, but expressed some skepticism as to whether this would suggest more aggressive rate cuts ahead. The latest policy communication by the PBoC seems to support our skepticism, as we do not see the more dovish language being echoed in the PBoC’s language, which maintains its slightly more hawkish tone on monetary policy support compared to last year (see QuickScan: Politburo Update December 2023 and QuickScan: CEWC Doubles Down on New Economy). Our Monetary Conditions Indicator (MoCI) also continues to suggest that monetary policy, while remaining accommodative, is unlikely to see substantially more easing in the current environment, making significant policy rate cuts less likely (see chart). Our analysis of the Politburo meeting in late April also suggested that policymakers appear to want fiscal policy to play a more active role going forward as compared to monetary policy (see DeepDive: Politburo Update April 2024).

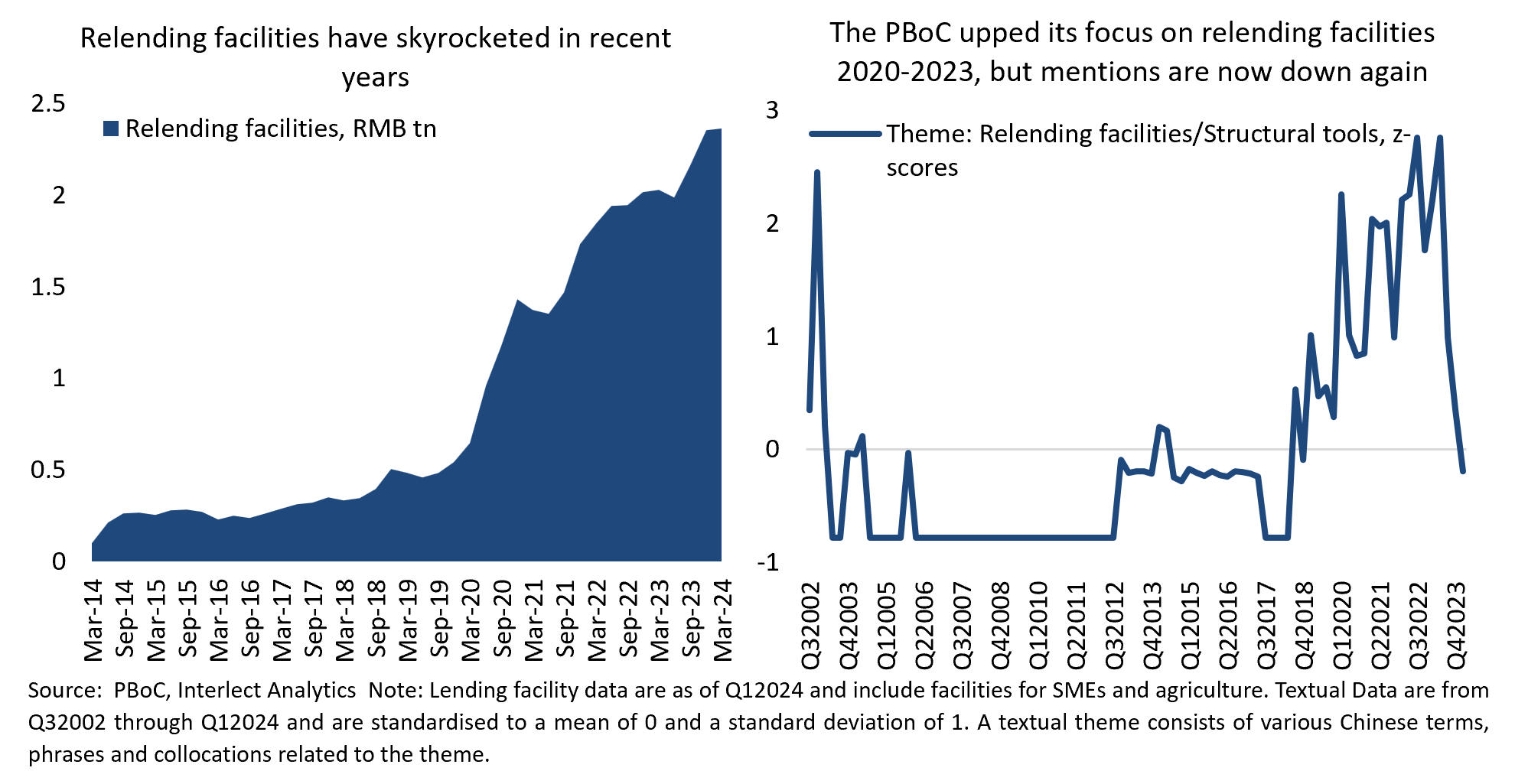

In recent years, the PBoC has made extensive use of relending facilities as part of its monetary policy toolbox. While we do see some more room for the facilities to be expanded, references to the programs in the monetary policy report have now fallen back to their long-term average, suggesting the pace of expansion could taper off in the coming quarters (see chart). Relending facilities are an important, but often overlooked, structural tool the PBoC has used to target certain pockets of the economy with preferential loan rates. Interest rates on these facilities have recently been as low as 1.75%, significantly below the one-year policy rate of 2.5%. (also see DeepDive: Politburo Update April 2024).

The PBoC also maintained its focus on optimising the use of existing loans to prevent an underutilisation of capital available in the financial system, an issue we discussed in QuickScan: Taking Stock of Money Supply Developments in August last year. It also warned against practices by banks to attract depositors with high interest rates on deposits. We believe these actions have, at least in part, contributed to the recent deceleration in broad money supply (M2), deposits and corporate loans, although the slowdown should also be seen within the context of the substantial expansion in both deposits and corporate loans in recent years (see DeepDive: Data Dump April 2024).

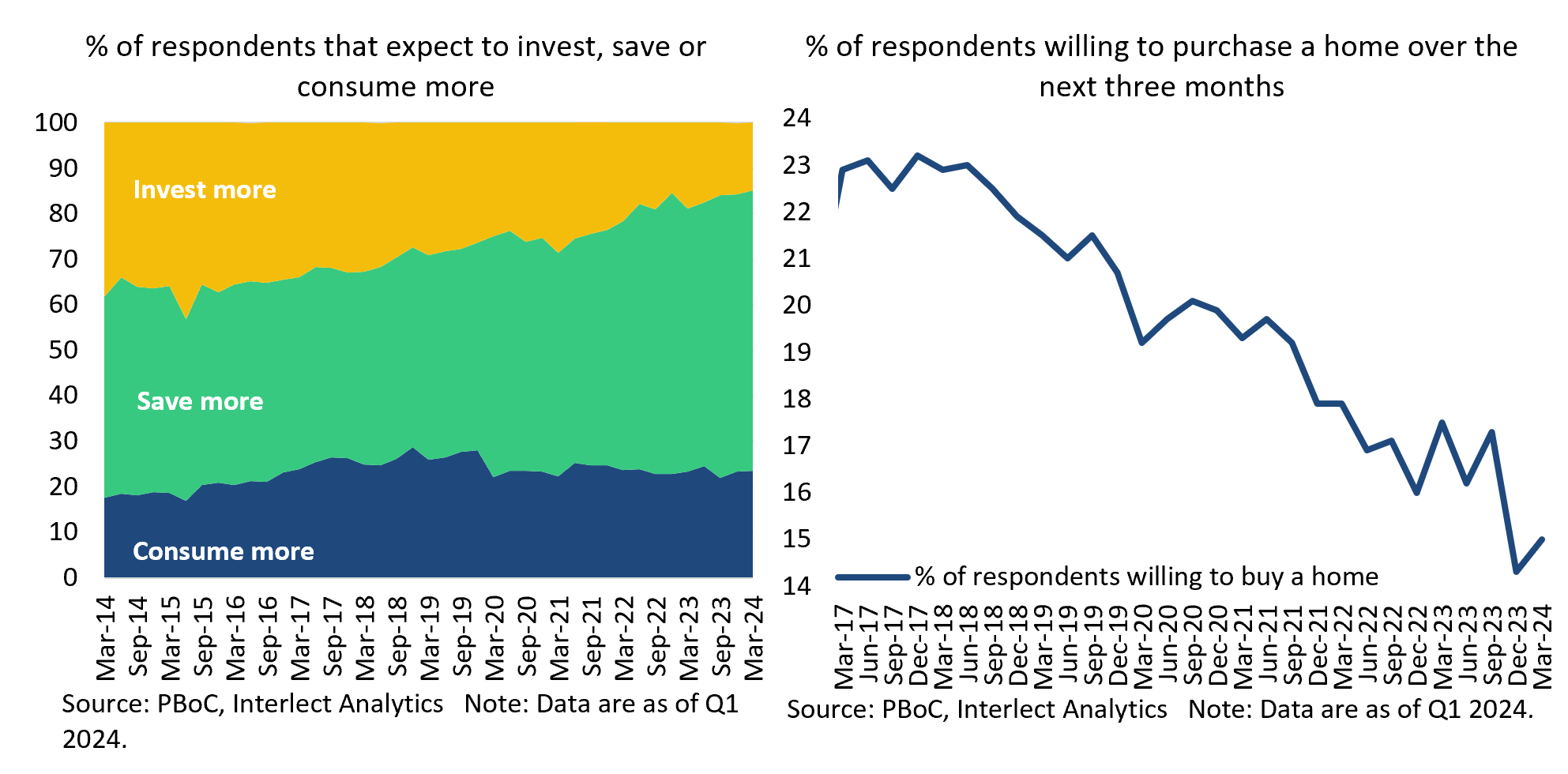

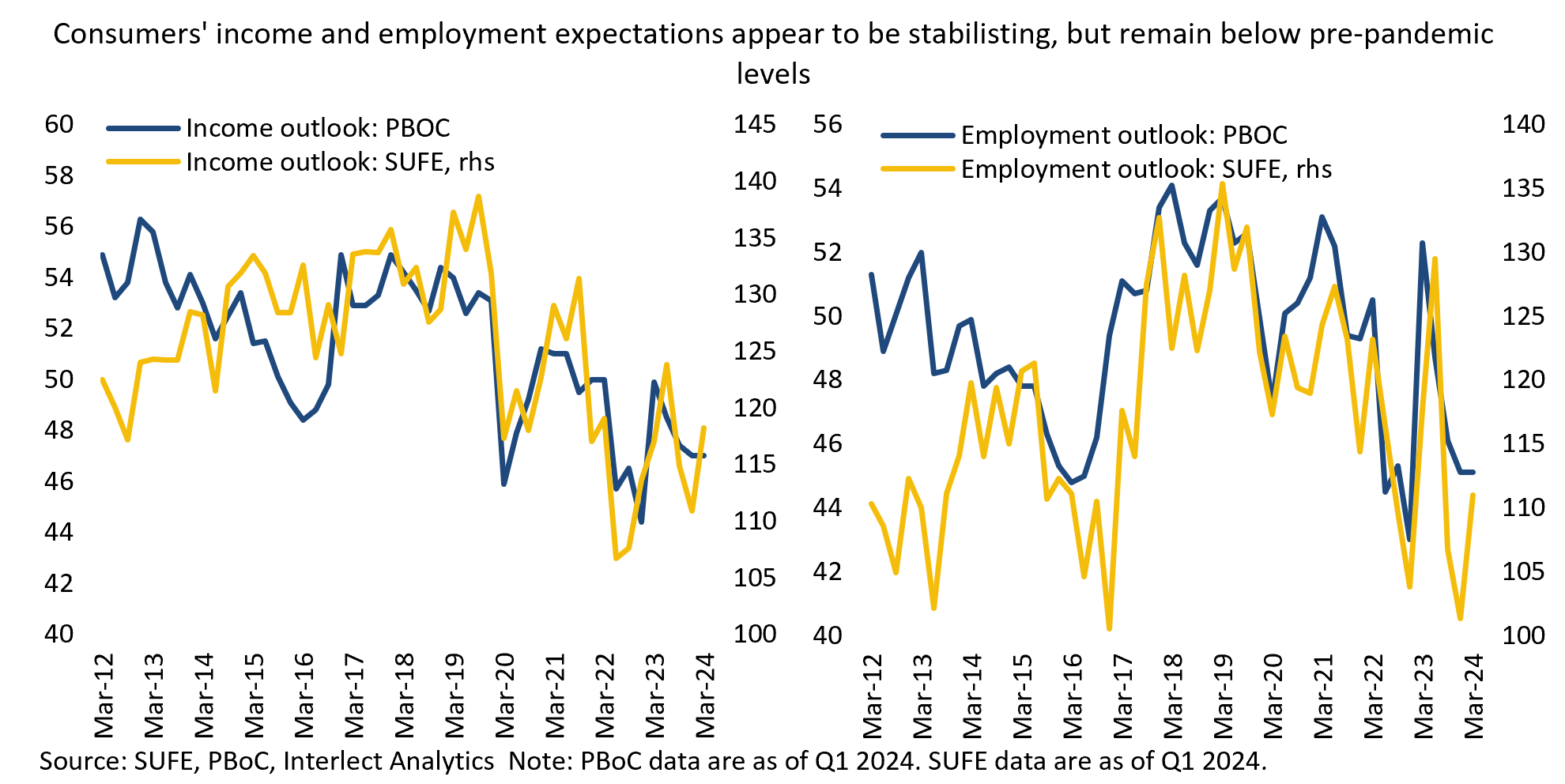

Among reasons for optimism, the PBoC cited improving confidence among consumers and corporates. While we are seeing some signs that business and consumer sentiment appears to be bottoming or stabilising, household consumption has been slow to recover (see DeepDive: Data Dump April 2024). The PBoC’s latest depositor survey for Q1 also suggests that consumers remain reluctant to increase spending, opting instead to save more (see chart). Household confidence remains fragile and still has a ways to go to recover.

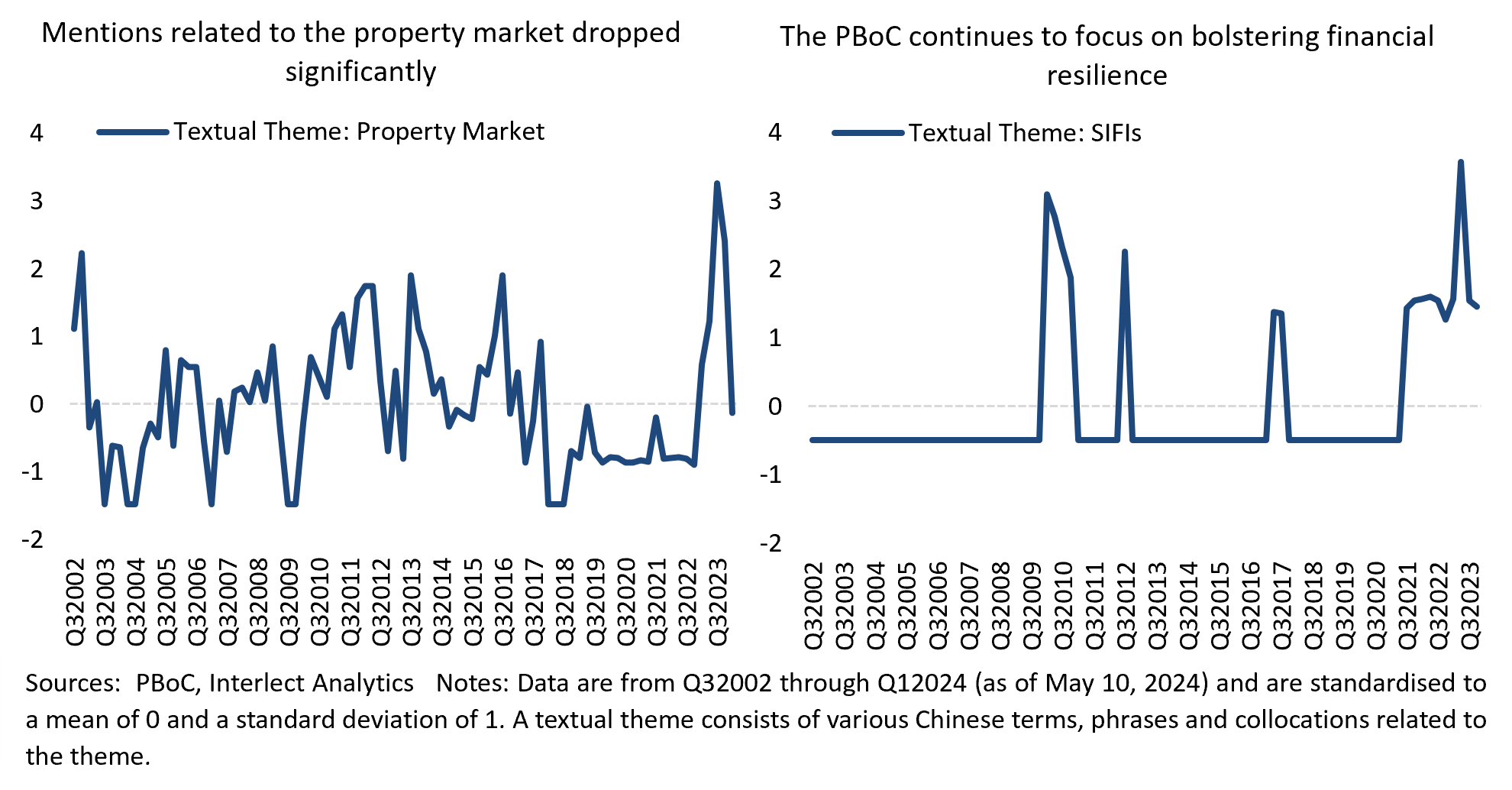

We noted a surprisingly strong drop in the PBoC’s focus on the property market compared to previous quarters, with the bank no longer singling out risks in the sector in its outlook. Although we do not think that risks have magically disappeared, as new home sales remain extremely weak and home prices continue to fall (see DeepDive: Data Dump April 2024), the drop may signal the PBoC is increasingly confident that risks are now manageable. However, since the magnitude of the drop truly took us by surprise, we would like to see some further confirmation in the PBoC’s policy communication going forward before drawing any conclusion. In our view, the housing market remains the most significant drag on the economy and household confidence.

Similarly, the central bank said it would like to see ongoing projects aimed at resolving existing financial risk to steadily come to an end, also indicating a growing confidence within the PBoC that risks are becoming more manageable. That said, mentions related to the need to improve the supervision of systemically important financial institutions (SIFIs) and China’s global systemically important banks (G-SIBs) remained elevated, with the PBoC still asking them to strengthen their total loss absorption capacities (TLAC). The PBoC has sustained its attention on SIFIs since the second half of 2021, marking the longest uninterrupted period of such focus dating back to at least 2002.

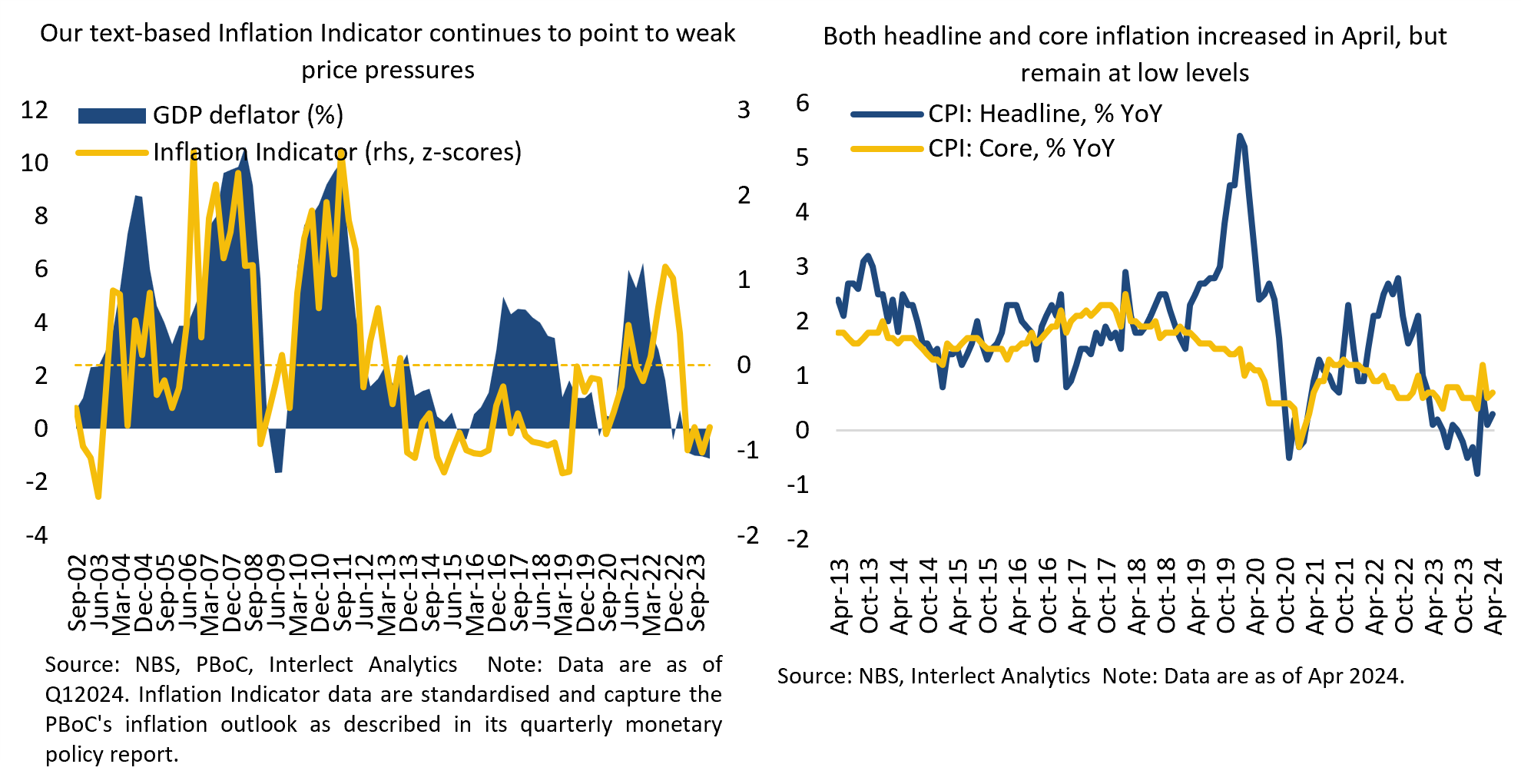

The PBoC reiterated its stance from earlier policy communications that inflation should increase moderately this year as the recovery picks up steam. We continue to see little inflationary pressure, as indicated by our text-based Inflation Indicator, which responds to concerns over inflationary risk. The GDP deflator, which is a broader measure of inflation than the CPI, has also been negative for four consecutive quarters. The PBoC also reiterated its view that monetary conditions remain appropriate and that the low inflationary environment is not a result of insufficient money supply. In our view, even small increases in the CPI will probably diminish the incentive for the PBoC to cut interest rates further, as a higher CPI would ‘mechanically’ help lower real financing costs further.

----------

This report has been prepared by Interlect Analytics Pte. Ltd. It is solely for information purposes and should not be taken as investment advice or a recommendation to buy or sell any security or investment product. Redistribution without prior consent is prohibited.