QuickScan: Can the External Macro Environment Prove to Be a Boon?

As we enter the new year, China’s domestic conditions continue to appear lacklustre. However, there are early indications of positivity in the external macro environment. Should these signals come to fruition, they could offer some much-needed support to the economy and industrials in the year ahead.

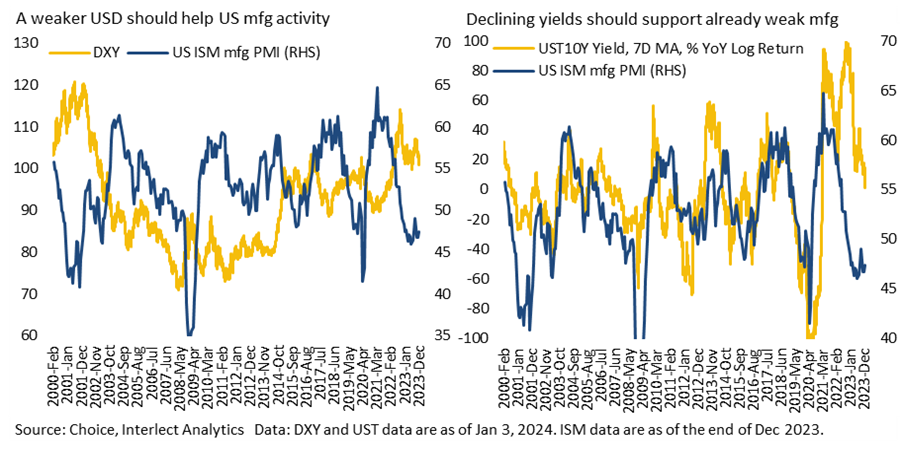

The USD has been losing some strength in recent months due to market expectations of lower interest rates, driven by a decrease in inflationary pressures. Historically, a weaker DXY and lower rates tend to have a favourable effect on US manufacturing activity.

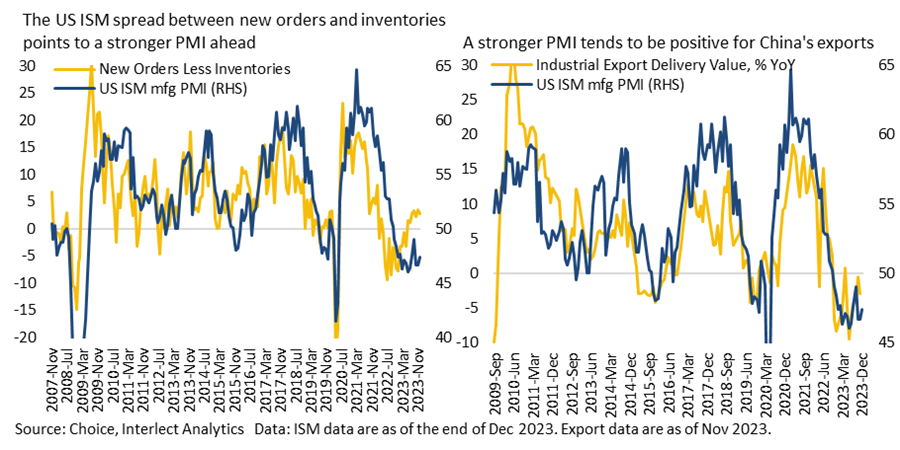

Despite the robust performance of the US economy last year, the purchasing managers’ index has, somewhat unexpectedly, remained in contraction territory. However, new orders, while still contracting, have shown some signs of improvement in recent months, while inventories remain low. A widening spread between the two typically indicates a forthcoming stronger PMI, which, in turn, should lend support to Chinese exports.

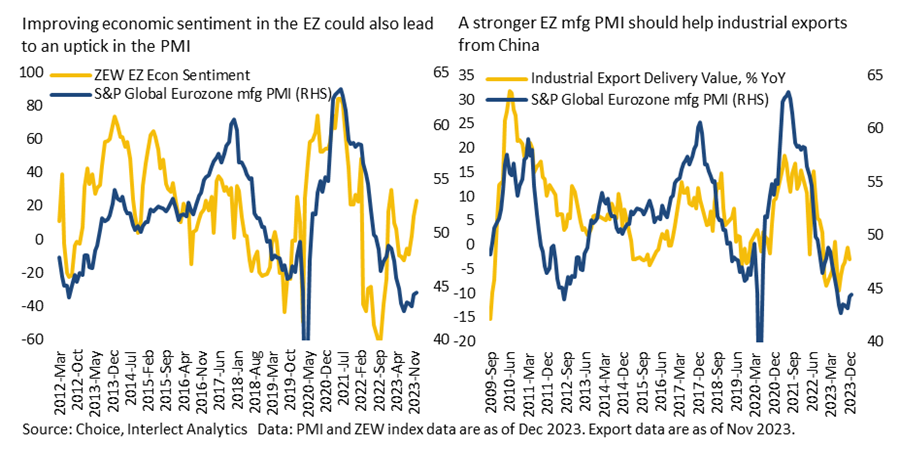

Sentiment in the eurozone has also been rising, as indicated by the ZEW Eurozone Economic Sentiment Index. While it may still be too soon to draw definite conclusions, should the PMI follow suit throughout the year, it could provide an additional boost to Chinese exports and industrials.

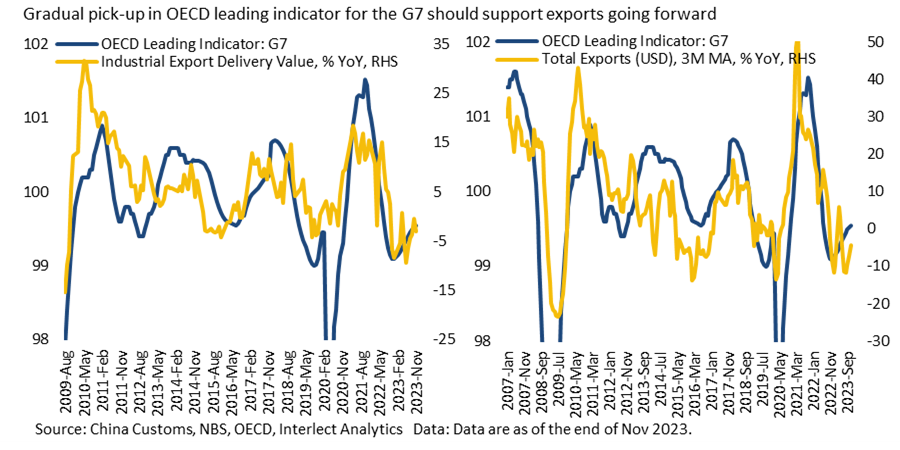

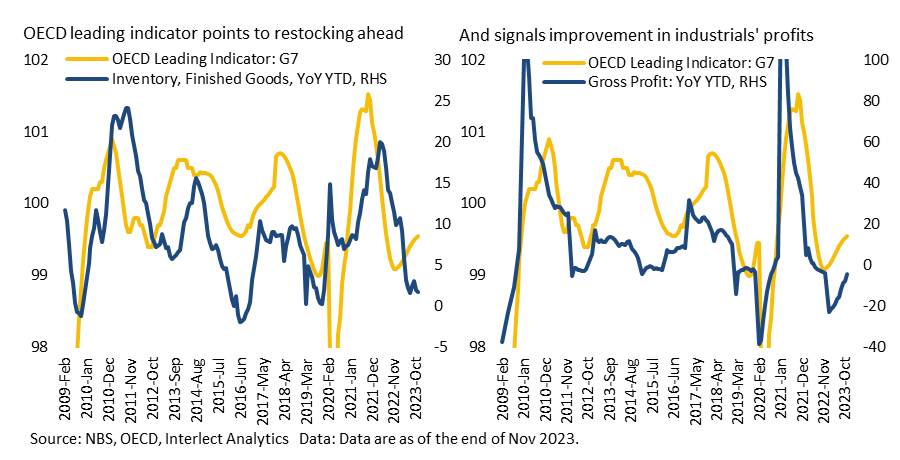

There are also some initial positive signals coming from the OECD leading indicator for G7 countries, which has been gradually reversing back towards its long-term average of 100. Although the G7’s share of China’s exports has been shrinking, the group remains its largest export market.

Improving external conditions, if continued, should help offset some of the domestic drag on the economy. Industrial inventories have been falling after a massive buildup in recent years and should improve going forward. Industrial profits should also be supported by a more positive external backdrop, especially among export-intensive firms.

In 2022, exports contributed roughly 38% to China’s industrial output. According to estimates by MofCom, the foreign trade sector accounts for about a quarter of China’s workforce, employing approximately 180 million people. We previously estimated that about 16% of the working population is directly or indirectly involved in export-related activities.

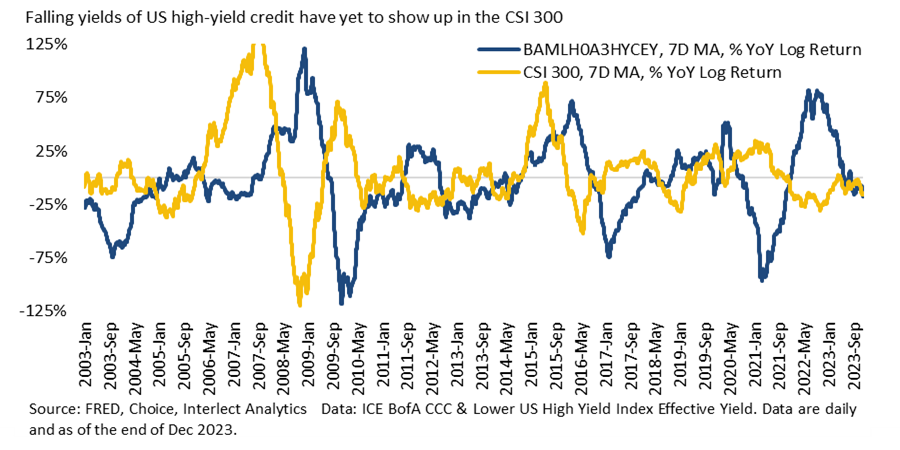

Yields of US corporate high-yield credit have also been coming down, which typically signals expectations of looser financial conditions and reduced financial stress. Historically, this has boded well for Chinese equities, as the two are negatively correlated.

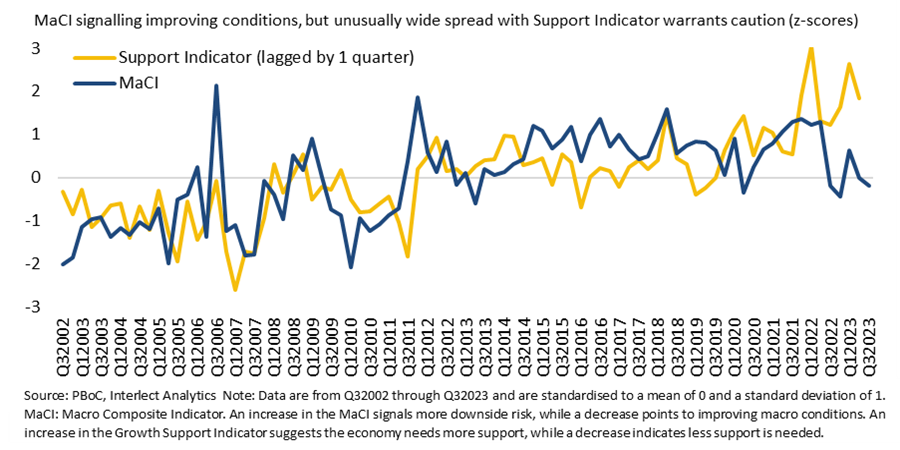

Our text-based PBoC macro conditions indicator (MaCI), on the other hand, has been sending mixed signals as to whether conditions in China are improving. While the indicator has been pointing to less downside risk, our growth support indicator, which historically has tracked the MaCI closely, has sharply diverged from it in recent quarters. The spread has been unusually wide, which, coupled with sluggish domestic demand, high deposit levels and housing market uncertainty, casts doubt on the overall economic outlook (see DeepDive: Key Messages from the PBoC’s Monetary Policy Outlook and DeepDive: Data Dump December 2023). In QuickScan: Politburo Update December 2023, we also noted a slightly more cautious tone on both monetary and fiscal support in recent policy communications. This hints at a somewhat more hawkish approach, barring any significant deterioration in the data.

Looking ahead, we think that external conditions appear more favourable, but domestic factors continue to weigh on the overall outlook, with persisting weakness in the property sector remaining a significant damper on demand and confidence. While certain pockets of the market, such as export-oriented manufacturing, may benefit from a more robust external environment, the broader outlook remains subdued until there are more tangible indications of a return of domestic confidence and demand.

----------

This report has been prepared by Interlect Analytics Pte. Ltd. It should not be taken as investment advice or a recommendation to buy or sell any security or investment product. Redistribution without prior consent is prohibited.